Installing JAGS

In addition to installing the jagsUI package, we also

need to separately install the free JAGS software, which you can

download here.

Once that’s installed, load the jagsUI library:

Typical jagsUI Workflow

- Organize data into a named

list - Write model file in the BUGS language

- Specify initial MCMC values (optional)

- Specify which parameters to save posteriors for

- Specify MCMC settings

- Run JAGS

- Examine output

1. Organize data

We’ll use the longley dataset to conduct a simple linear

regression. The dataset is built into R.

data(longley)

head(longley)

# GNP.deflator GNP Unemployed Armed.Forces Population Year Employed

# 1947 83.0 234.289 235.6 159.0 107.608 1947 60.323

# 1948 88.5 259.426 232.5 145.6 108.632 1948 61.122

# 1949 88.2 258.054 368.2 161.6 109.773 1949 60.171

# 1950 89.5 284.599 335.1 165.0 110.929 1950 61.187

# 1951 96.2 328.975 209.9 309.9 112.075 1951 63.221

# 1952 98.1 346.999 193.2 359.4 113.270 1952 63.639We will model the number of people employed (Employed)

as a function of Gross National Product (GNP). Each column

of data is saved into a separate element of our data list. Finally, we

add a list element for the number of data points n. In

general, elements in the data list must be numeric, and structured as

arrays, matrices, or scalars.

2. Write BUGS model file

Next we’ll describe our model in the BUGS language. See the JAGS manual for detailed information on writing models for JAGS. Note that data you reference in the BUGS model must exactly match the names of the list we just created. There are various ways to save the model file, we’ll save it as a temporary file.

# Create a temporary file

modfile <- tempfile()

#Write model to file

writeLines("

model{

# Likelihood

for (i in 1:n){

# Model data

employed[i] ~ dnorm(mu[i], tau)

# Calculate linear predictor

mu[i] <- alpha + beta*gnp[i]

}

# Priors

alpha ~ dnorm(0, 0.00001)

beta ~ dnorm(0, 0.00001)

sigma ~ dunif(0,1000)

tau <- pow(sigma,-2)

}

", con=modfile)3. Initial values

Initial values can be specified as a list of lists, with one list

element per MCMC chain. Each list element should itself be a named list

corresponding to the values we want each parameter initialized at. We

don’t necessarily need to explicitly initialize every parameter. We can

also just set inits = NULL to allow JAGS to do the

initialization automatically, but this will not work for some complex

models. We can also provide a function which generates a list of initial

values, which jagsUI will execute for each MCMC chain. This

is what we’ll do below.

4. Parameters to monitor

Next, we choose which parameters from the model file we want to save

posterior distributions for. We’ll save the parameters for the intercept

(alpha), slope (beta), and residual standard

deviation (sigma).

params <- c('alpha','beta','sigma')5. MCMC settings

We’ll run 3 MCMC chains (n.chains = 3).

JAGS will start each chain by running adaptive iterations, which are

used to tune and optimize MCMC performance. We will manually specify the

number of adaptive iterations (n.adapt = 100). You can also

try n.adapt = NULL, which will keep running adaptation

iterations until JAGS reports adaptation is sufficient. In general you

do not want to skip adaptation.

Next we need to specify how many regular iterations to run in each

chain in total. We’ll set this to 1000 (n.iter = 1000).

We’ll specify the number of burn-in iterations at 500

(n.burnin = 500). Burn-in iterations are discarded, so here

we’ll end up with 500 iterations per chain (1000 total - 500 burn-in).

We can also set the thinning rate: with n.thin = 2 we’ll

keep only every 2nd iteration. Thus in total we will have 250 iterations

saved per chain ((1000 - 500) / 2).

The optimal MCMC settings will depend on your specific dataset and model.

6. Run JAGS

We’re finally ready to run JAGS, via the jags function.

We provide our data to the data argument, initial values

function to inits, our vector of saved parameters to

parameters.to.save, and our model file path to

model.file. After that we specify the MCMC settings

described above.

out <- jags(data = jags_data,

inits = inits,

parameters.to.save = params,

model.file = modfile,

n.chains = 3,

n.adapt = 100,

n.iter = 1000,

n.burnin = 500,

n.thin = 2)

#

# Processing function input.......

#

# Done.

#

# Compiling model graph

# Resolving undeclared variables

# Allocating nodes

# Graph information:

# Observed stochastic nodes: 16

# Unobserved stochastic nodes: 3

# Total graph size: 74

#

# Initializing model

#

# Adaptive phase, 100 iterations x 3 chains

# If no progress bar appears JAGS has decided not to adapt

#

#

# Burn-in phase, 500 iterations x 3 chains

#

#

# Sampling from joint posterior, 500 iterations x 3 chains

#

#

# Calculating statistics.......

#

# Done.We should see information and progress bars in the console.

If we have a long-running model and a powerful computer, we can tell

jagsUI to run each chain on a separate core in parallel by

setting argument parallel = TRUE:

out <- jags(data = jags_data,

inits = inits,

parameters.to.save = params,

model.file = modfile,

n.chains = 3,

n.adapt = 100,

n.iter = 1000,

n.burnin = 500,

n.thin = 2,

parallel = TRUE)While this is usually faster, we won’t be able to see progress bars when JAGS runs in parallel.

7. Examine output

Our first step is to look at the output object out:

out

# JAGS output for model '/tmp/Rtmp32mRJh/fileab4a797205d3', generated by jagsUI.

# Estimates based on 3 chains of 1000 iterations,

# adaptation = 100 iterations (sufficient),

# burn-in = 500 iterations and thin rate = 2,

# yielding 750 total samples from the joint posterior.

# MCMC ran for 0.001 minutes at time 2026-01-29 15:20:58.879265.

#

# mean sd 2.5% 50% 97.5% overlap0 f Rhat n.eff

# alpha 51.845 0.797 50.250 51.819 53.444 FALSE 1 1.005 465

# beta 0.035 0.002 0.031 0.035 0.038 FALSE 1 1.005 471

# sigma 0.729 0.145 0.508 0.707 1.067 FALSE 1 1.000 750

# deviance 33.487 2.871 30.032 32.781 40.779 FALSE 1 1.002 750

#

# Successful convergence based on Rhat values (all < 1.1).

# Rhat is the potential scale reduction factor (at convergence, Rhat=1).

# For each parameter, n.eff is a crude measure of effective sample size.

#

# overlap0 checks if 0 falls in the parameter's 95% credible interval.

# f is the proportion of the posterior with the same sign as the mean;

# i.e., our confidence that the parameter is positive or negative.

#

# DIC info: (pD = var(deviance)/2)

# pD = 4.1 and DIC = 37.614

# DIC is an estimate of expected predictive error (lower is better).We first get some information about the MCMC run. Next we see a table

of summary statistics for each saved parameter, including the mean,

median, and 95% credible intervals. The overlap0 column

indicates if the 95% credible interval overlaps 0, and the

f column is the proportion of posterior samples with the

same sign as the mean.

The out object is a list with many

components:

names(out)

# [1] "sims.list" "mean" "sd" "q2.5" "q25"

# [6] "q50" "q75" "q97.5" "overlap0" "f"

# [11] "Rhat" "n.eff" "pD" "DIC" "summary"

# [16] "samples" "modfile" "model" "parameters" "mcmc.info"

# [21] "run.date" "parallel" "bugs.format" "calc.DIC"We’ll describe some of these below.

Diagnostics

We should pay special attention to the Rhat and

n.eff columns in the output summary, which are MCMC

diagnostics. The Rhat (Gelman-Rubin diagnostic) values for

each parameter should be close to 1 (typically, < 1.1) if the chains

have converged for that parameter. The n.eff value is the

effective MCMC sample size and should ideally be close to the number of

saved iterations across all chains (here 750, 3 chains * 250 samples per

chain). In this case, both diagnostics look good.

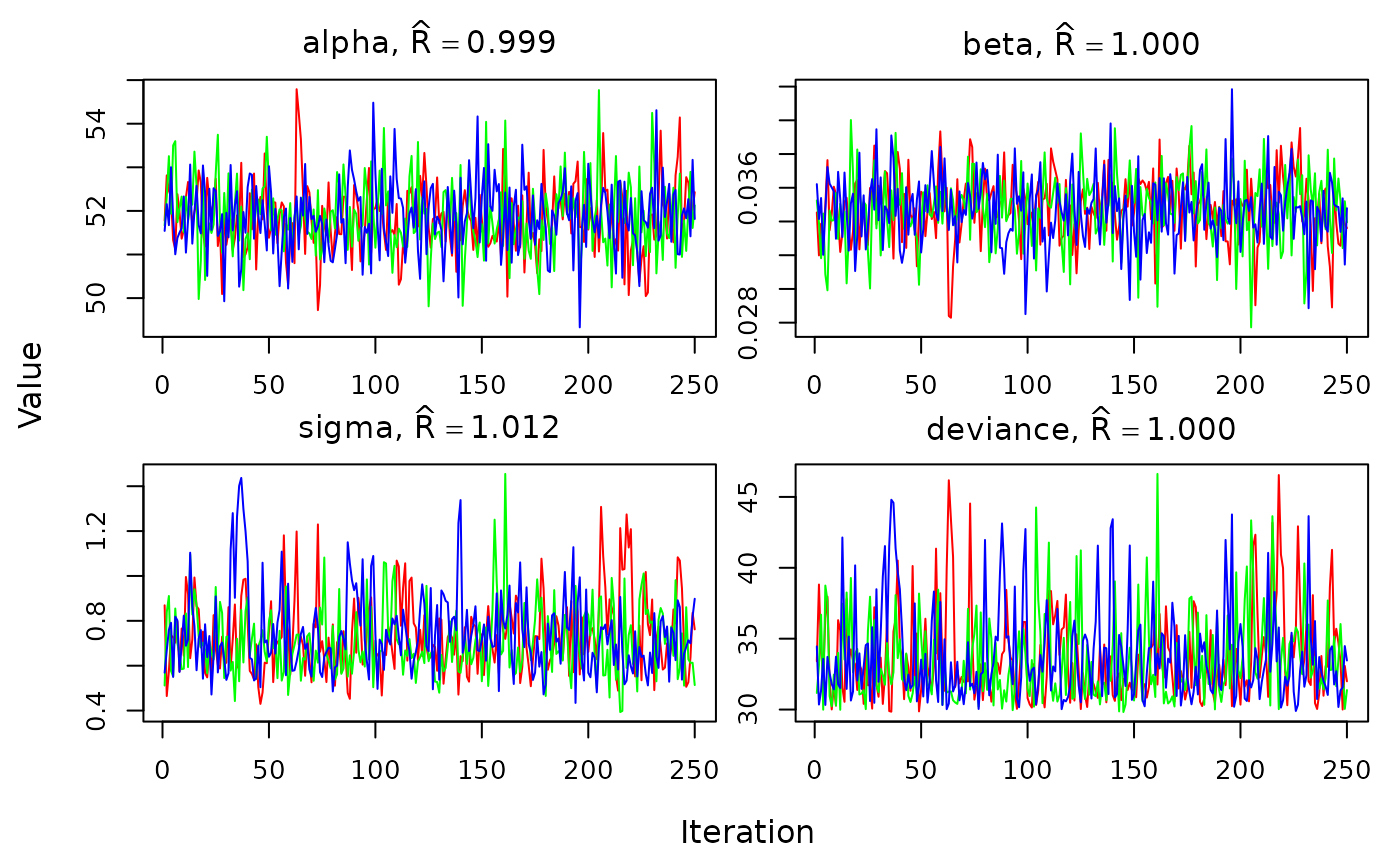

We can also visually assess convergence using the

traceplot function:

traceplot(out)

We should see the lines for each chain overlapping and not trending up or down.

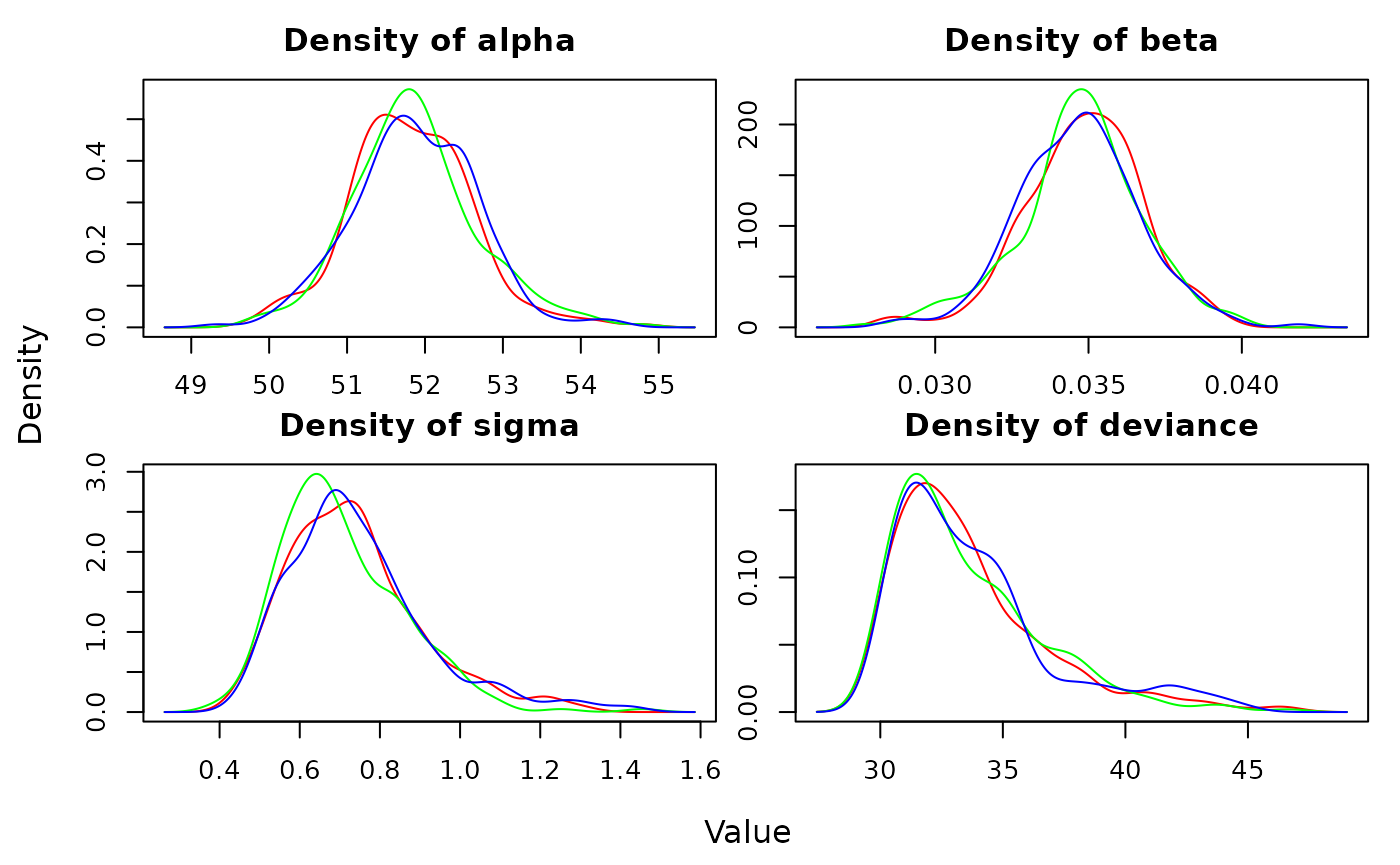

Posteriors

We can quickly visualize the posterior distributions of each

parameter using the densityplot function:

densityplot(out)

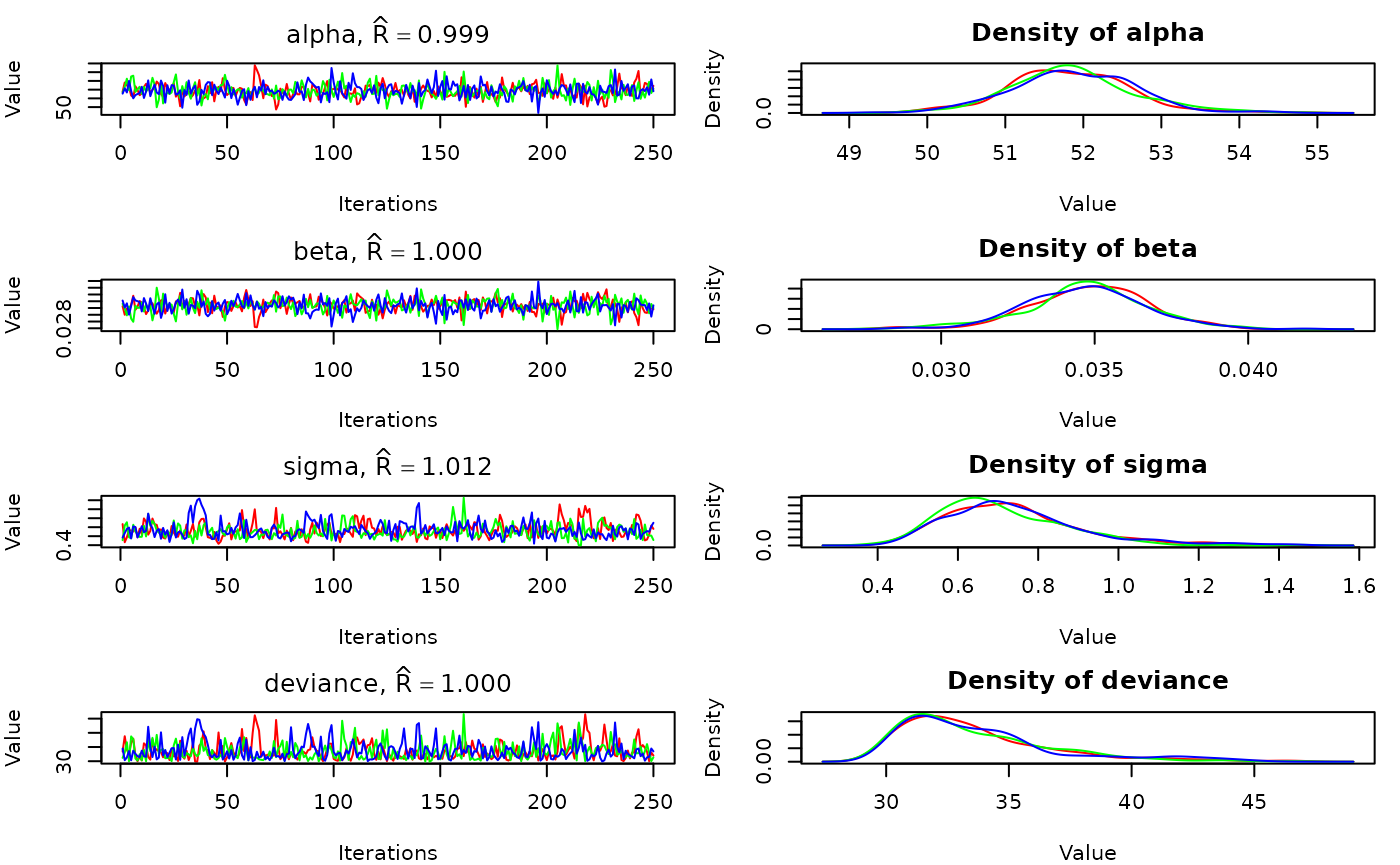

The traceplots and posteriors can be plotted together using

plot:

plot(out)

We can also generate a posterior plot manually. To do this we’ll need

to extract the actual posterior samples for a parameter. These are

contained in the sims.list element of out.

post_alpha <- out$sims.list$alpha

hist(post_alpha, xlab="Value", main = "alpha posterior")

Update

If we need more iterations or want to save different parameters, we

can use update:

# Now save mu also

params <- c(params, "mu")

out2 <- update(out, n.iter=300, parameters.to.save = params)

# Compiling model graph

# Resolving undeclared variables

# Allocating nodes

# Graph information:

# Observed stochastic nodes: 16

# Unobserved stochastic nodes: 3

# Total graph size: 74

#

# Initializing model

#

# Adaptive phase.....

# Adaptive phase complete

#

# No burn-in specified

#

# Sampling from joint posterior, 300 iterations x 3 chains

#

#

# Calculating statistics.......

#

# Done.The mu parameter is now in the output:

out2

# JAGS output for model '/tmp/Rtmp32mRJh/fileab4a797205d3', generated by jagsUI.

# Estimates based on 3 chains of 1300 iterations,

# adaptation = 100 iterations (sufficient),

# burn-in = 1000 iterations and thin rate = 2,

# yielding 450 total samples from the joint posterior.

# MCMC ran for 0 minutes at time 2026-01-29 15:20:59.484717.

#

# mean sd 2.5% 50% 97.5% overlap0 f Rhat n.eff

# alpha 51.828 0.771 50.365 51.806 53.435 FALSE 1 1.003 450

# beta 0.035 0.002 0.031 0.035 0.038 FALSE 1 1.003 450

# sigma 0.730 0.157 0.504 0.700 1.131 FALSE 1 1.027 87

# mu[1] 59.985 0.353 59.328 59.982 60.704 FALSE 1 1.003 450

# mu[2] 60.860 0.313 60.288 60.860 61.474 FALSE 1 1.003 450

# mu[3] 60.812 0.315 60.234 60.812 61.430 FALSE 1 1.003 450

# mu[4] 61.736 0.277 61.220 61.732 62.300 FALSE 1 1.003 450

# mu[5] 63.281 0.225 62.839 63.278 63.727 FALSE 1 1.002 450

# mu[6] 63.909 0.210 63.490 63.911 64.327 FALSE 1 1.002 450

# mu[7] 64.549 0.200 64.165 64.547 64.936 FALSE 1 1.002 450

# mu[8] 64.470 0.201 64.086 64.469 64.860 FALSE 1 1.002 450

# mu[9] 65.666 0.197 65.299 65.656 66.033 FALSE 1 1.003 450

# mu[10] 66.422 0.206 66.037 66.420 66.807 FALSE 1 1.004 450

# mu[11] 67.243 0.224 66.804 67.238 67.657 FALSE 1 1.005 450

# mu[12] 67.305 0.226 66.859 67.299 67.722 FALSE 1 1.005 450

# mu[13] 68.634 0.270 68.096 68.629 69.166 FALSE 1 1.005 450

# mu[14] 69.326 0.298 68.763 69.321 69.918 FALSE 1 1.005 450

# mu[15] 69.868 0.321 69.265 69.864 70.527 FALSE 1 1.005 450

# mu[16] 71.147 0.380 70.422 71.141 71.922 FALSE 1 1.004 450

# deviance 33.533 2.941 30.202 32.717 40.939 FALSE 1 1.030 82

#

# Successful convergence based on Rhat values (all < 1.1).

# Rhat is the potential scale reduction factor (at convergence, Rhat=1).

# For each parameter, n.eff is a crude measure of effective sample size.

#

# overlap0 checks if 0 falls in the parameter's 95% credible interval.

# f is the proportion of the posterior with the same sign as the mean;

# i.e., our confidence that the parameter is positive or negative.

#

# DIC info: (pD = var(deviance)/2)

# pD = 4.2 and DIC = 37.77

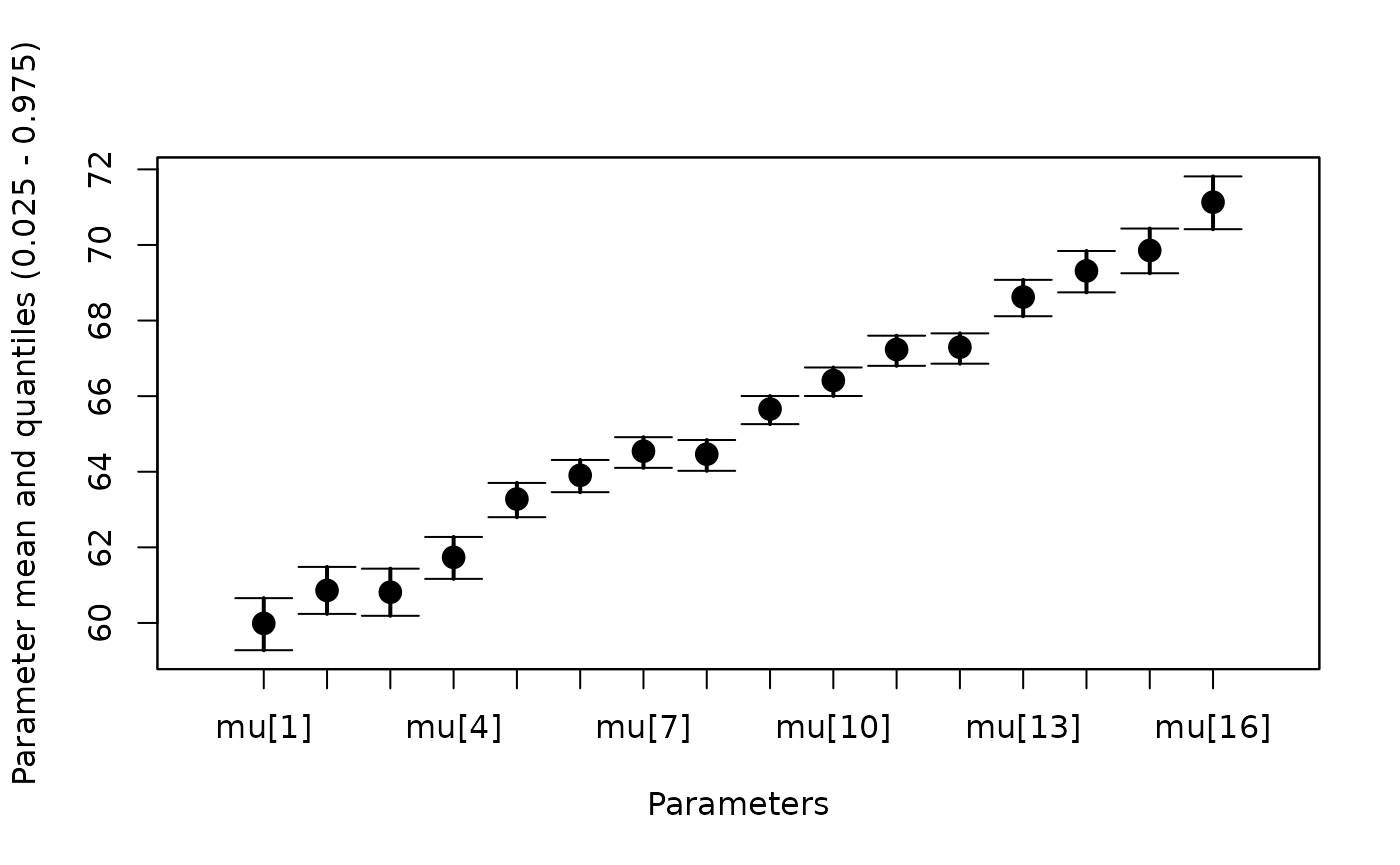

# DIC is an estimate of expected predictive error (lower is better).This is a good opportunity to show the whiskerplot

function, which plots the mean and 95% CI of parameters in the

jagsUI output:

whiskerplot(out2, 'mu')